Curve.fi is the prominent example of a protocol that has seen sustained success, prompting others to adopt a tokenomics model based on vote escrowed tokens. By tying CRV to veCRV, Curve was the first to implement these mechanisms, giving token holders access to three essential functions:

- Voting on which farm will receive token emissions.

- Earning staking rewards.

- token timelocking to increase such rewards. As a result of being locked, these tokens cannot be traded or tokenized.

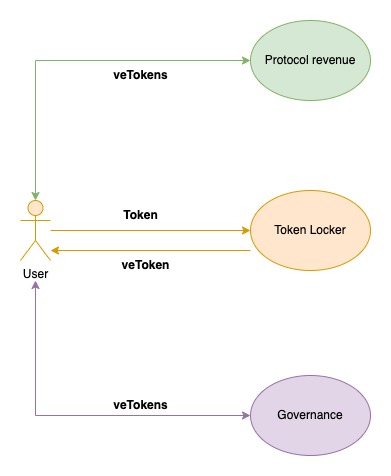

The following diagram illustrates how this model can be generalized:

Summary of the Vote Escrow Tokenomics System

Getting the right to vote on how new CRV tokens are released has been a key part of Curve’s economy. With Curve’s technology, stablecoin swap slippage is kept to a minimum, which makes transactions cheaper. Because of this, DeFi protocols that issue stablecoins want to have Curve pools. If CRV token emissions can be redirected to a pool, liquidity providers in those pools will get more rewards, which will bring in more liquidity. More liquidity will make swap slippage even less likely and help a stablecoin stay tied to its pair. These stablecoin protocols usually get seigniorage fees for releasing their stablecoins, so keeping their stablecoins closely tied to the dollar is important if they want investors to use and hold their stablecoins.

Curve uses one of the most important ideas in veTokenomics, which is that the weight of a vote and the amount of rewards are both related to the timelock. This means that people who lock the protocol token for longer will get more rewards, up to 2.5 times more rewards if they lock it for the maximum of 4 years. Many people now think that this method might work better in some situations than the old “1 token = 1 vote” system.

Incentives for locking the token

By locking the protocol token for the given amount of time, the token holder shows that they are committed to the protocol during that time. Also, it lowers the number of tokens in circulation, which could make it harder to sell the main token. With the voting power that comes with vested tokens, you can vote every so often on where the tokens will be sent. Each pool gets a certain percentage of the total rewards. The people who own the locked token, i.e., veToken vote on each reward share. Here is the Dune dashboard, which shows current guage allocations for the Curve protocol:

https://dune.com/queries/1319548

Gauge weights

It’s important to know that in the Curve protocol, protocol token staking rewards don’t come from token dilution, but from the trading fees. In the case of Curve, tokens are given out to people who provide liquidity. Curve charges a swap fee of 0.04%, of which 50% goes to liquidity providers and 50% goes to veCRV holders. This means that half of the fees generated so far by the protocol have been distributed towards veCRV holders, which is an attractive incentive for users to lock their tokens. For the protocol like Curve, this fee amount is very huge.

Curve Wars

According to IntoTheBlock Curve metrics, the total fees and volume of Curve Finance as of January 16, 2023

Understanding these power plays explains the so-called “Curve wars,” where users can deposit liquidity provider tokens from Curve that will be maximally locked by a protocol like Convex finance ($18.44bn TVL). By doing this, Curve’s liquidity providers can receive additional CVX ( Protocol token for Convex finance) rewards without having to lock their tokens in the platform. Approximately half of the circulating supply of veCRV is currently held by Convex.

Curve made this model of tokenomics popular, but there are a lot of other protocols that have already added similar features or plan to do so in the future. Andre Cronje and his cofounder also devised ve (3, 3), an improvement on ve-tokenomics. In ve ( 3, 3 ), veTokens are liquid through NFTs. Separate article incoming for ve ( 3, 3 ) tokenomics.

This is a good tokenomics model for methods of issuing tokens that want a token with real power to make decisions and real use as a value-adding asset. In the veTKN architecture, timelocks and regular token releases make it less meaningful to sell the primary token. The idea also encourages long-term stakes and active participation in DAO proposals, both of which have been wanted for a long time because many DAO votes have low quorums. Despite these benefits, some critics say this approach looks like a plutocratic, tiered structure that relies on bribery and governance, which may not be in line with how the crypto ecosystem started. Only systems that are easy to use and actually work, will last, simple!

Leave a Reply